- Concerns surrounding higher-for-longer interest rates, a lack of speculative appetite, weakening physical demand amid Chinese economic weakness, and slowing US growth, suggest the silver market is set to be looser than the projected 110Moz annual deficit this year. Very high carry costs and elevated lease rates should see more metal pushed onto the market, loosening primary markets. This will be augmented by muted physical investment and industrial demand, as the US economy slows to a crawl and Chinese economic weakness continues. Consequently, silver is unlikely to break much above US$23-24/oz for the next several months.

- As it becomes clearer, in late-2023, that the Fed and other central banks will start to pivot to a more dovish monetary policy in Q1 2024, we expect the white metal to start setting its sights on US$26/oz. Lower interest rates, firmer physical investment, and recovering industrial demand will work together to tighten supply-demand fundamentals. Our price projections are roughly in line with the median market consensus for the next several months, but they are some US$2-3 higher six to nine months out, with an upside risk.

- In the very long-term, silver is expected to trade significantly above the US$26/oz mark and should increasingly decouple from gold as its ties to the interest/lease rate environment weaken. As the global electrification transformation takes root, demand from solar panels and auto electronics is set to continue outpacing supply, which will drain inventories to levels that will make it difficult to balance the market left short by poor growth from mining and recycling.

Primary deficits don’t guarantee strong silver prices

After materially outperforming gold for much of late-2020 to mid-2021 and late-2022, silver has underwhelmed for about a year now. In 2020, prices jumped 27% to an annual average of US$20.55/oz, which was followed by another 22% surge to US$25.14/oz in 2021. However, the price dropped 13% to a US$21.73/oz annual average last year.

Last year’s decline occurred despite the fact that silver demand reached a record 1.242Boz, driven by a 5% increase in industrial demand, a 22% jump in physical investment, a 29% jump in jewellery uptake, and an 80% surge in silverware usage. The consequent record deficit of 238Moz was insufficient to prevent the price decline in 2022.

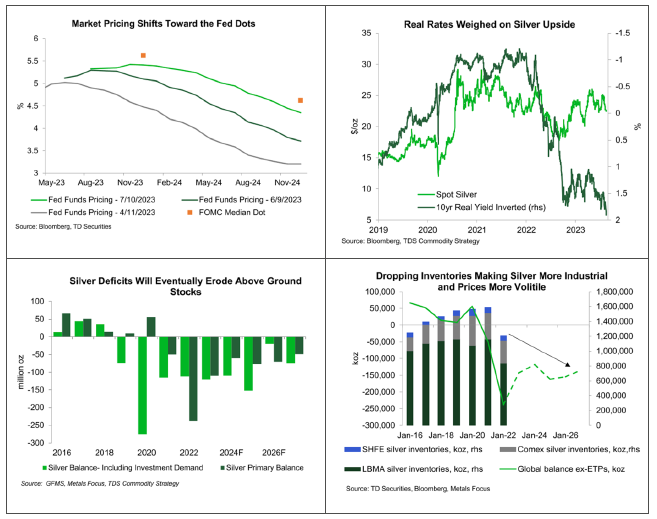

Notwithstanding an expected late-year bounce in industrial and physical investment demand, alongside another deep annual deficit of about 110Moz projected for this year, silver is currently trending at just above a modest below US$24/oz. Interest rate-driven institutional investment flows, which tilted positioning toward shorts, are overpowering expectations of stronger physical investment and industrial demand later in the year.

For now, the projected deep deficit is being overwhelmed by the highest interest rates in over two decades, as also occurred back in 2022. Investment and interest rate-driven physical inventory flows often trump tight primary physical market conditions.

Silver’s monetary and industrial metal properties a negative for now

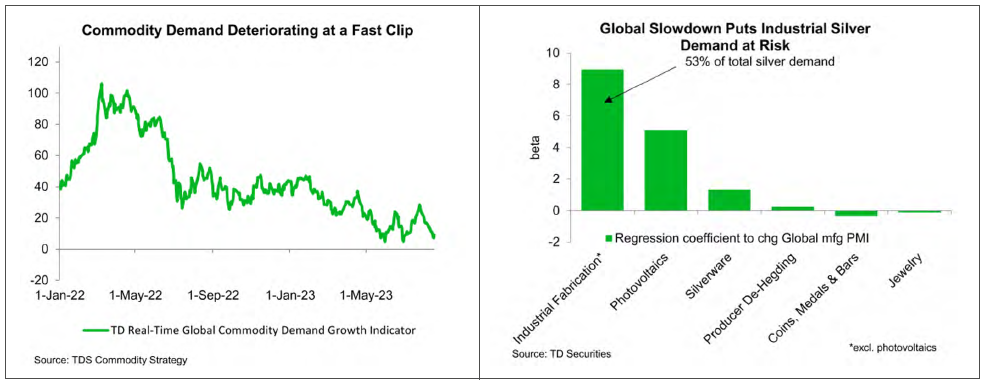

Since the white metal behaves both as an industrial and a monetary metal, it reacts negatively to elevated interest rates and industrial demand weakness. Investors have little appetite to build long positions when rates are projected to rise or stay at restrictive levels. They also tend to reduce length, when the economy is set to slow materially, as this implies less uptake by the industrial sector.

Both Chinese and US data are pointing toward industrial activity weakness. Market participants are worried that hawkish monetary policy signals coming from key central banks and weakening industrial activity across the globe will loosen supply-demand fundamentals over the next few months, despite the projected primary shortfall for the year as a whole.

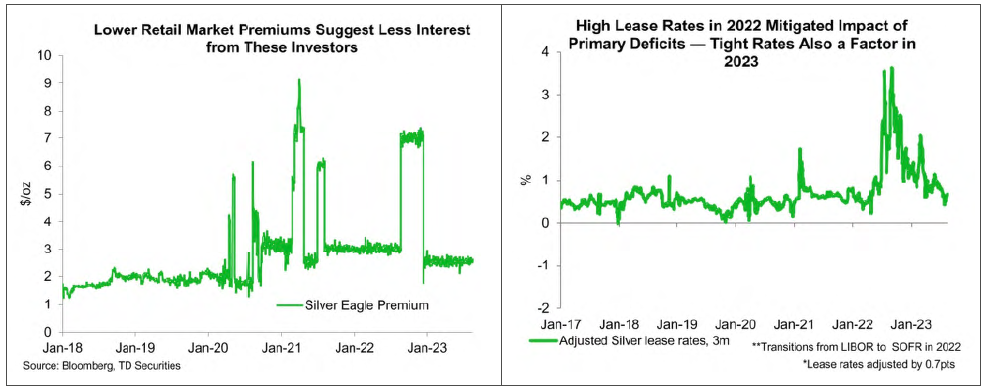

High interest rates, modest speculative appetite, and slumping physical demand suggest that lease rates may be at levels high enough to attract a significant amount of metal into the market. Meanwhile, higher carry costs are also likely to see metal being pushed onto the market, or may significantly reduce interest in new long acquisitions.

Despite the fact that the consensus is calling for another robust shortfall between what is produced by miners and recyclers, and what is consumed this year, we argue that the roughly 1.3Boz of inventory (of which 60-70% is unallocated) can more than fill any potential shortfall in the coming months. These dynamics will likely limit silver price upside over the next few years, despite projected deficits.

Lease rates and the cost-of-carry move metal in and out of the market, based on the opportunity cost associated with holding the asset. Hence, a high interest rate environment (as the world is currently experiencing), should direct more metal into the market, which should place a cap on silver prices over much of our forecast horizon.

Of course, demand weakness stemming from a deteriorating macroeconomic environment is also a key reason why prices are set to be weaker than many silver enthusiasts hoped. We also believe that the pending US recession and Chinese economic weakness will limit physical investment and industrial demand. As such, silver is projected to trend on either side of US$23-24/oz for much of the next few months.

Dovish pivot, economic recovery a big positive for silver amid deficits

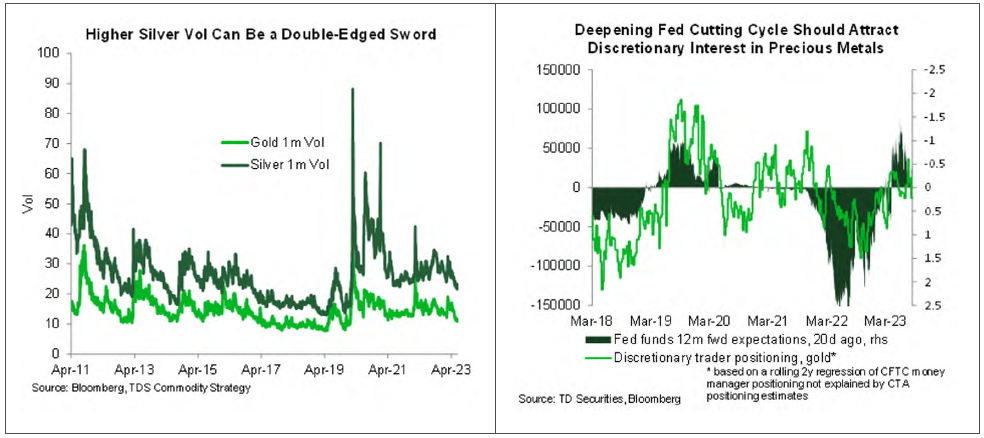

However, a reversal of hawkish monetary policy signals should help catalyze more supportive flows in the latter part of the year, after it becomes clear that the Fed and other central banks will pivot to a more dovish monetary policy stance. We judge the actual policy tilt toward a more dovish stance will start in March 2024, but markets should react positively many months before this happens. This typically helps gold, but silver should benefit too, as it also is a monetary metal, albeit less so. So, markets will be watching the Fed’s every move, particularly discretionary investors.

Once an economic recovery is on the horizon, the white metal should get an additional boost from the industrial side, which could see it target US$26/oz in the latter part of 2023 and early-2024. At that time, interest rates, firmer physical investment, ETP purchases, and industrial demand will work together to tighten market conditions.

Since silver has a high beta to gold, with double the rate of volatility, it is projected to outperform during this phase of the rally. The precious metals complex typically reacts long before the actual cuts in rates occur, which implies that long exposure may start to drive prices materially higher in the late part of the third quarter.

We argue that this relationship occurs because as rates drop, the cost of carry, opportunity, and lease rates all reduce the metal available to physical markets. Lower carry and opportunity costs imply that inventories held by bullion banks and investors are likely to rise, as the pressure to swap or lease metal to markets moderates. There will also be more discretionary investment in futures and physical ETPs, which have shown to be a big driver of prices over the years.

Uptake by silver ETPs will reduce the available metal for industrial use, coins, and other retail products, which is consistent with facts on the ground recently and tends to contribute to higher prices. Back in 2020 and 2021, large inflows into silver ETPs were consistent with very robust silver market rallies, likely helped by unusually low interest rates. This is in sharp contrast to 2022, when some 126Moz flowed out of these funds, helping to mute the primary deficit and to drive prices lower. Further, 2022 also saw a sharp rise of rates along the yield curve.

Considering that rates are set to remain at over a two-decade high through this year, there will be plenty of metal available from above ground stocks to help offset the tightness coming from the some 110Moz annual deficit. However, as markets start to perceive that monetary policy will pivot to the dovish side, market participants will react well ahead of the actual early-2024 rate cuts. For that reason, we project the price recovery to take root in Q4-2023.

Electrification, paltry mine CAPEX a mana for silver long-term

Silver has traditionally behaved like a hybrid metal, exhibiting characteristics of a pure monetary metal, like gold, and those found in base metals, such as copper. It was often the case that even when the primary supply (mined and recycled) was outpaced by industrial and physical investment demand in coins and bars, prices did not necessarily rally as was the case in 2022. The reason for this was that interest rates (cost of carry and opportunity cost to hold), and lease rates provide incentives to move metal to physical markets from inventory.

Up to now, there has always been metal available from investor pools to supply the market. Today, at 1.2Boz in inventory (some 70% available to be allocated at will) there is plenty of metal available to close supply gaps which may appear, which was the case many times over the last decade.

However, as demand associated with the electrification of the global economy grows, in order to fight climate change, it looks like the world will face persistent primary silver deficits over the long-term. Silver uptake by the emerging EV industry, smart devices, electrical grids, solar power generation, and the conventional industrial products looks set to outpace the quantities produced by miners and recyclers.

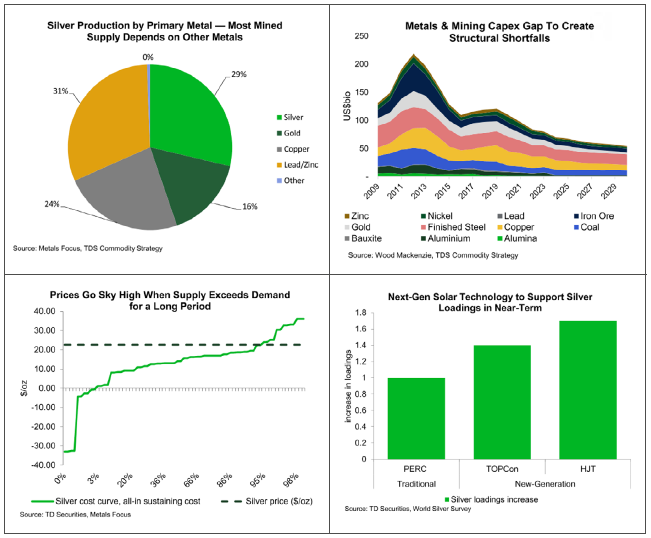

There are relatively few primary silver projects in the cards, which will limit mined metal growth. Even more importantly, mined byproduct silver supply is set to have a modest pace of growth over the next decade or so. Byproduct mines provide some 72% of all primary silver, and the lack of investment there suggests modest growth in silver production from zinc, lead, copper, and gold miners into the next decade.

At the same time, recycled metal growth will be limited in the expansion phase of electrification, as most of the uses will be new and these products will have a considerable life span before they become candidates for recycling.

If deficits persist for a prolonged period as expected, the inventory of above-ground stocks will diminish to levels which will be too low to consistently provide the buffer against them. This implies very high prices, as the silver sector will operate above the conventional supply curve (mined and recycled metals).

This suggests that prices will be determined by an auction of sort, where this market will be balanced by demand destruction for a period. This, in turn, implies that price will not be determined by the standard supply-demand equilibrium, but rather prices will clear above that conventional cost curve. We expect that at over the period of excess demand, prices will be set by the opportunity cost a user faces by giving up a marginal unit of silver to the market. While we don’t know where that is exactly, we can say with a high level of confidence it will be above the 100th percentile on the cost curve, which now sits at US$36/oz.

A lack of available above ground inventories will also likely make the white metal more of an industrial metal, less driven by the interest rate environment, and more by pure supply-demand fundamentals. As inventories erode relative to demand, volatility should increase as well.

{kind=link}