I have recently been arguing that the global investment landscape is experiencing a “paradigm shift”, mirrored by very significant changes in regulation and business priorities. Dictionary definitions of a “paradigm shift” usually describe it as a fundamental change in the basic concepts, approach or underlying assumptions of a discipline, and this seems a fair definition of the major structural transformation currently reshaping investment and business strategies. We are currently witnessing the major realignment of priorities and expectations around environmental, social and governance (ESG) issues, and 2022 is increasingly looking like a milestone year – perhaps a tipping point.

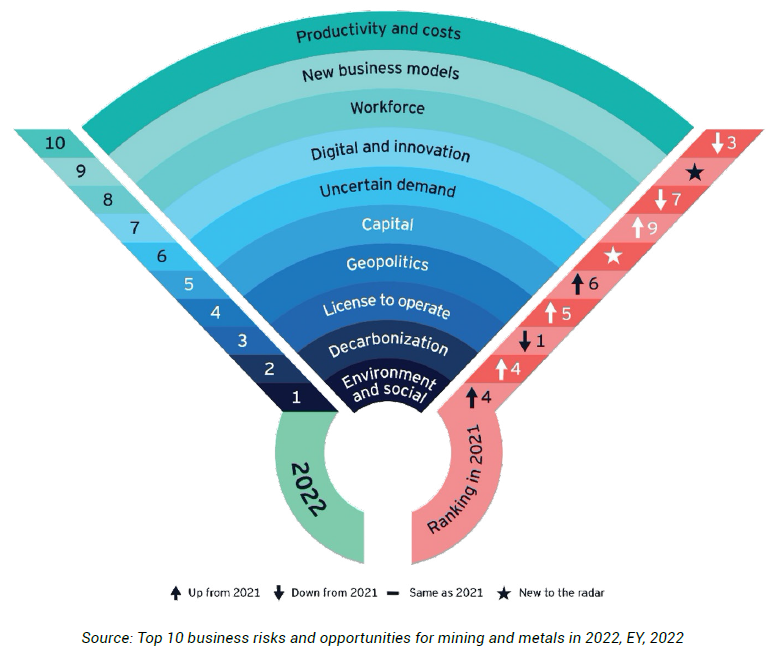

This shift has some very major implications for the mining sector. Fortunately, there are strong indications that many industry leaders are mindful of changing expectations and the expanding set of risks and opportunities they present. EY’s annual survey of metals and mining business risks and opportunities saw the sector’s C-suite rank “Environmental and social factors”, “Decarbonization”, and “Licence to operate” as the three most pressing issues facing their businesses in 2022.

There have been many suggestions in recent years that the industry is being transformed and, as the ESG agenda becomes embedded in corporate objectives, it is very likely to accelerate this transformation.

For some industry participants and stakeholders, this as a natural progression – an evolution of the motivations and goals previously articulated and expressed via a focus on the CSR (Corporate Social Responsibility) outputs and altruistic or philanthropic activities of companies. But the sheer scale and speed of the recent change, driven in part by investors’ response to the climate crisis, suggests something more radical, more akin to a revolution – a structural realignment of priorities and purpose. This is also reflected in the focus of attention and interventions from policy makers and regulators.

There are now many indicators and proof points to support this view. Surveying the regulatory landscape, the UN-backed Principles of Responsible Investment (PRI) reports that the first half of 2021 saw the introduction of 159 new or revised responsible investment policy instruments (more than the total for the previous year).

Many of these policy initiatives are rapidly moving from industry-specific “good practice” guidelines towards being mandatory obligations. As institutional investors seek to reweight their asset allocations and redirect capital to support their ESG objectives, they have also been making louder calls for better data from companies and more consistent reporting mechanisms to allow them to make more informed decisions.

One of the most significant trends of recent years has been the emergence of a wide range of ESG and sustainability reporting frameworks and standards. While there is much debate as to the consistency, scope and overlap of these initiatives, there have been efforts to harmonize them and it is highly likely they will continue to converge, as indicated by the formation of the International Sustainability Standards Board (ISSB) late last year.

And corporate performance on key ESG factors, as reported under these frameworks, is increasingly being consolidated and summarized by ratings and indexing suppliers as they seek to “productize” their measurement of companies’ performance.

The mining industry, if it is not to be left behind, needs to respond to these demands and, wherever possible, move to greater transparency and consistency in how it reports on its wider environmental and social impacts. It is worth noting, however, that the underlying data collection processes and measurement methodologies employed by ESG rating agencies have been developed quite rapidly. There is a question, therefore, as to whether they have been produced with sufficient knowledge of (or sensitivity to) particular sectors to be an accurate representation of current corporate actions and intentions. The mining and metals sector may have some cause for concern here.

It was the need to ensure that gold mining can demonstrate, in a clear and consistent fashion, that it operates to very high standards of performance across a wide range of ESG factors that led the World Gold Council to develop the Responsible Gold Mining Principles. These principles are increasingly recognized across the industry as a comprehensive and credible framework that enables companies to demonstrate with confidence that their gold has been produced responsibly. They are mandatory for our member companies – most of the world’s forward-thinking gold mining companies – and, importantly, they are independently assured.

Some companies may, understandably, feel uncomfortable with mandatory disclosure rules being imposed upon them, but there is growing evidence that such disclosure obligations may have significant benefits. For example, research last year (from the European Corporate Governance Institute and the Swiss Finance Institute) found that, “Mandatory ESG reporting helps to improve a firm’s financial information environment: analysts’ earnings forecasts become more accurate and less dispersed after ESG disclosure becomes mandatory. On the real side, negative ESG incidents become less likely, and stock price crash risk declines, after mandatory ESG disclosure is enacted.”

The assumption behind many market participants and commentators resistant to integrating ESG objectives into corporate purpose is that will impose a substantial burden on business. But the early acknowledgment of social and environmental factors as potential systemic risks can help companies develop robust plans and responses. The reorienting of business objectives, to include the development of plans and solutions to address ESG factors, will very likely present new opportunities and attract new investors.

A range of analytical and academic work now points to the positive correlations between ESG performance and company resilience and value. Recently, for example, financial analytics provider MSCI Inc. concluded a four-year study on this issue and found that companies with high ESG scores experienced lower costs of capital, lower equity costs, and lower debt costs compared to companies with poor ESG scores. And experts at McKinsey, citing more than 2,000 academic studies, concluded that better ESG scores translate to around a 10% lower cost of capital, while reflecting lower regulatory, environmental, and litigation risks.

Mining has already started to demonstrate it can adapt to this paradigm shift

One of the pre-requisites in seeking to address climate and sustainability challenges – a key aspect of the ESG paradigm shift – is the need for longer-term perspectives and commitments. Climate change in particular requires risk scenarios and plans that stretch across decades. Whereas investors, even those charged with implementing long-term strategies, often struggle with horizons that extend beyond five years, or 10 years at an extreme stretch.

There is now a growing wealth of evidence to support the thesis that this short-termism is a problematic feature of market behaviour that demands our attention, and data from both individual firms and the wider economy suggest that such behaviour is value-destructive. Research also suggests that the growing focus on ESG-conscious business – and the associated investor scrutiny – may, however, help counter the market’s more myopic tendencies.

Mining is, of course, a very long-term business. It should therefore, with good management and governance, be well aligned with the shift in time horizons that will be needed if investors adapt to the new paradigm.

The widespread demands for greater clarity and evidence of plans and actions on sustainability factors have coalesced around the recommendations of the Taskforce on Climate-related Financial Disclosures (TCFD). This is, in part, because climate change is now recognized as the most significant challenge to global stability and prosperity and is already having very severe destructive impacts on the earth’s eco-systems.

The global economy will have to adapt to both build resilience against climate impacts and to rapidly reduce its greenhouse gas emissions to avoid the most catastrophic impacts. Some commentators may still view the management of these issues as primarily the responsibility of governments, but this perspective will likely result in a failure to recognize the very substantial value-creative opportunities in adapting to the transitioning economy.

It is now widely recognized that far more metals will be needed to deliver the infrastructure needed by a net-zero-carbon economy. How mining companies adapt themselves to deliver this material, while also seeking to minimize negative impacts, will be crucial to how they are judged and valued by investors and wider society.

While climate-related risks and decarbonization strategies may have garnered most recent attention, there is also a growing acknowledgement of the need for progress on the wider ESG agenda.

The need for greater market recognition of the value of the natural environment and bio-diversity, coupled with strategies to prevent further nature loss, has led, for example, to the launch of the Taskforce on Nature-related Financial Disclosures (TNFD), already endorsed by G7 Finance Ministers and the G20 Sustainable Finance Roadmap.

More broadly still, use of the UN Sustainable Development Goals (SDGs) as a valuable reference framework by which investors may measure corporate and sectoral performance on a wide range of ESG objectives has also gained considerable traction recently.

I think it significant, and perhaps also surprising to many industry outsiders, that leading mining companies are already not only demonstrating an awareness of the SDGs, but also reporting on their contributions to progress on specific goals. For example, we recently published a summary of a wide range of gold mining company activities, with positive impacts, focused on advancing the goals.

Looking forward, it is almost certain that the trends I’ve described above will continue to gain momentum. Pressure will grow for boards to be able to demonstrate they understand and are adequately prepared to address ESG issues. Global ESG-related standards will continue to evolve and converge in 2022. And further efforts, including regulations, will be directed towards the drive for greater accountability, integrity and consistency on corporate and sectoral ESG performance. Finally, investor and societal expectations will rapidly shift from the recent focus on longer-term commitments (such as net zero 2050 decarbonization pledges) to nearer-term actions and impacts.

Mining has already started to demonstrate it can adapt to this paradigm shift and it needs to continue and accelerate its progress. It also needs to learn how to tell the story of its transformation in a clearer, more compelling way, and to a wider audience so that they may better understand mining’s role in delivering solutions to many of the world’s urgent needs

{kind=link}