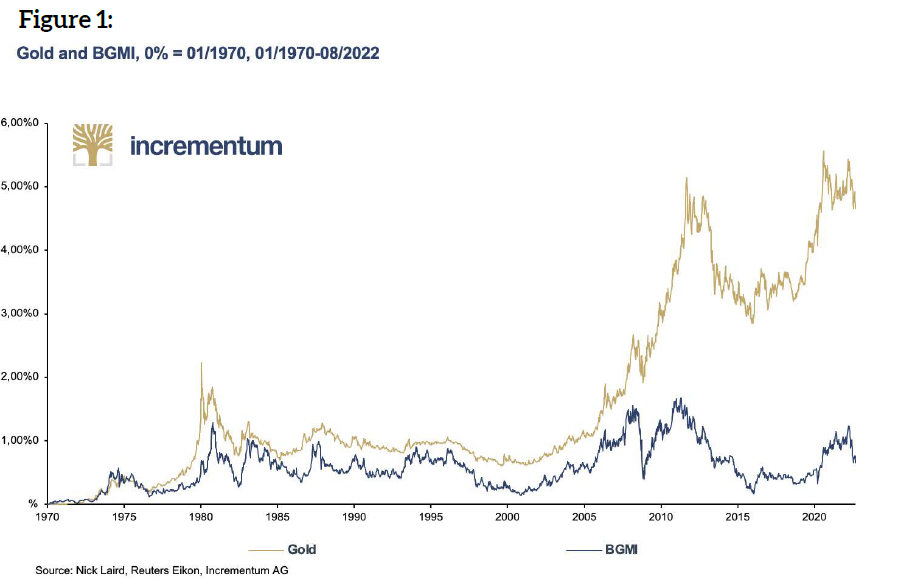

The following chart (Figure 1) shows the long-term development of gold prices and the Barron’s Gold Mining Index (BGMI). As can be seen, the difference in yield has widened over the years to a very high level. While between January 1970 and December 2021 the gold price increased by 4,667%, the BGMI grew by “only” 658%. The difference in performance was relatively small for decades. However, over the last 15 years the situation has changed rapidly. The gold miners have lagged behind the gold price.2

Why the poor performance of the gold miners? Actually, there are several reasons. The main factors that need to be mentioned are CAPEX overruns, growing production costs, environmental constraints and problems with permitting, governments wanting a bigger share of the pie, and political instability, as well as declining reserves and a chronic lack of new “major discoveries”.

Environmental constraints and problems with permitting

Permitting a mine is becoming ever more challenging. Even in mining-friendly countries, the procedure is becoming increasingly complex and time-consuming. Thus, obtaining permits takes ever more effort and resources.

Resource nationalism: governments want a (much) bigger share of the pie

Another problem miners have to face are growing government demands. In developed countries it is harder and harder to get a mine permitted; but at least, after permission is granted and the mine built, ownership rights are well protected. On the other hand, in emerging and developing countries it is often easy to build a mine; however, it is harder to keep it, as governments want bigger and bigger shares of the pie. Besides increasing production taxes, they sometimes decide to seize a mine.

Political instability

Politics does not impact the miners only through higher taxes and mine seizures. For example, Africa has recently been hit by a wave of coups. In 2021, coups occurred in Mali, Sudan, Guinea, and Chad, and also Burkina Faso in January 2022. The coups bring a lot of insecurity, as they are usually accompanied by some violence that may escalate rather quickly.

Share dilution

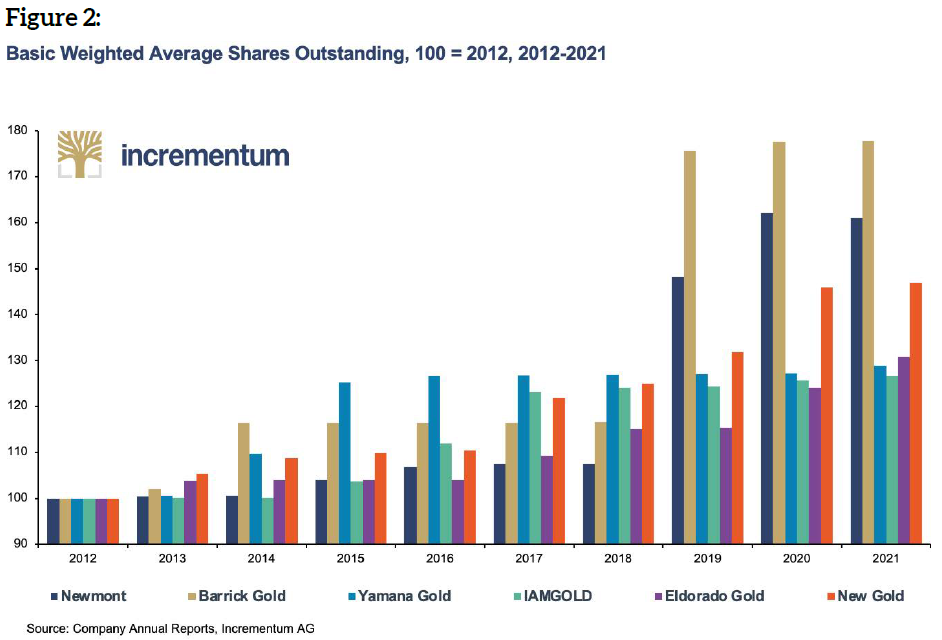

Another potential problem is share dilution. For mining companies, equity financing is often the only option for financing common operations and further development of mining projects. The negative impacts of share dilution are most visible in the case of the explorers and junior miners. They often have only very limited access to other financing options; and due to the risky nature of their business, they often have to undergo equity financings at very unfavourable terms. That means they must issue new shares at very low prices, and they often have to add some warrants in order to attract more investors. As a result, their share counts may grow by hundreds of percent in only a few years.

The chart above, (Figure 2) demonstrates that share dilution also impacts the bigger players in the gold mining industry. They are less dependent on equity financings, as they have much better access to debt financing. However, they often use shares as compensation for their managers and directors. And, sometimes, they encounter operational issues, and as their debt capacity is exhausted, equity financing is the only option for getting out of trouble. Moreover, the mining companies commonly pay for acquisitions of new projects or whole companies with their shares.

Declining reserves and number of new discoveries

A big problem of the gold mining sector is the declining number of new gold discoveries, regardless of the volume of exploration budgets.3 As shown in the chart below, although exploration budgets are more than twice as high as in the 1990s or early 2000s, the volume of discovered gold is much smaller. This means that in general it has become significantly more expensive to discover an ounce of gold. As a result, it has become more and more difficult – and also more expensive – for the gold miners, especially the big ones, to replenish the extracted ounces.

CAPEX overruns

A study prepared by McKinsey and PDAC investigated 41 gold mines established between 2008 and 2018 that had a CAPEX of US$0.5B or higher.4 According to their results, only 20% of investigated projects experienced no cost overruns. On the other hand, 44% of projects experienced 15-100% cost overruns, and 19% of projects suffered even greater than 100% cost overruns.

Growing production costs

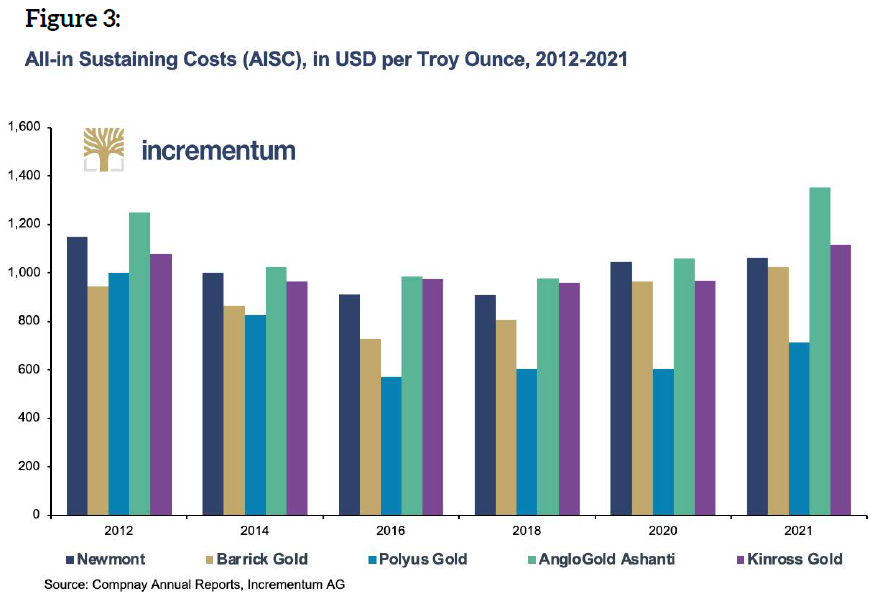

A similar problem is growing production costs. This indicator is hard to follow on a longer time span, because the generally accepted methodology of reporting production costs, AISC, was adopted only in 2012. Today, the biggest gold miners, except for Polyus Gold, have AISC in the US$1,000t/oz range. But only 20 years ago, in 2002, the gold price was around US$300t/oz. Therefore the AISC had to be below US$300t/oz. At the current AISC, the whole industry would have been dead.

The next chart (Figure 3) shows the development of AISC of major gold producers between 2012 and 2021. Between 2012 and 2016, the miners were able to push AISC down. Declining gold prices helped as well, as a lower gold price means that the miners pay lower royalties. Moreover, declining gold prices forced some of the higher-cost miners to suspend some operations or to re-evaluate their mining plans and focus on high-grade sections of the deposits. Of course, this cannot be done forever.

This trend was exacerbated by the COVID-19 pandemic, as some miners had to interrupt production, which pushed production volumes lower and production unit costs higher.

Moreover, over the past year or two, energy prices increased significantly, construction materials prices did too, and inflation came roaring back; thus, we may expect that escalating wage demands are only a matter of time. Add to this higher gold prices and therefore higher royalties to be paid by the miners, declining gold grades and the need to extract gold from greater depths or from deposits located in remote places with extreme weather conditions, and we could see an AISC of over US$1,000t/oz become the new normal.

The current inflation environment and related challenges

The last two factors, CAPEX overruns and growth of production costs, are poised to be especially haunting to the mining industry in the foreseeable future. The reason is that the genie of inflation has escaped the bottle.

According to a study by Goldmoney, the biggest operating cost of the top gold miners is labour (39%), followed by fuel and power (20%), consumables (20%), maintenance (11%), and other costs (10%).5 Fuel and energy costs have already increased. Given current inflation levels, investors should be prepared for gold production costs to keep on growing for some time.

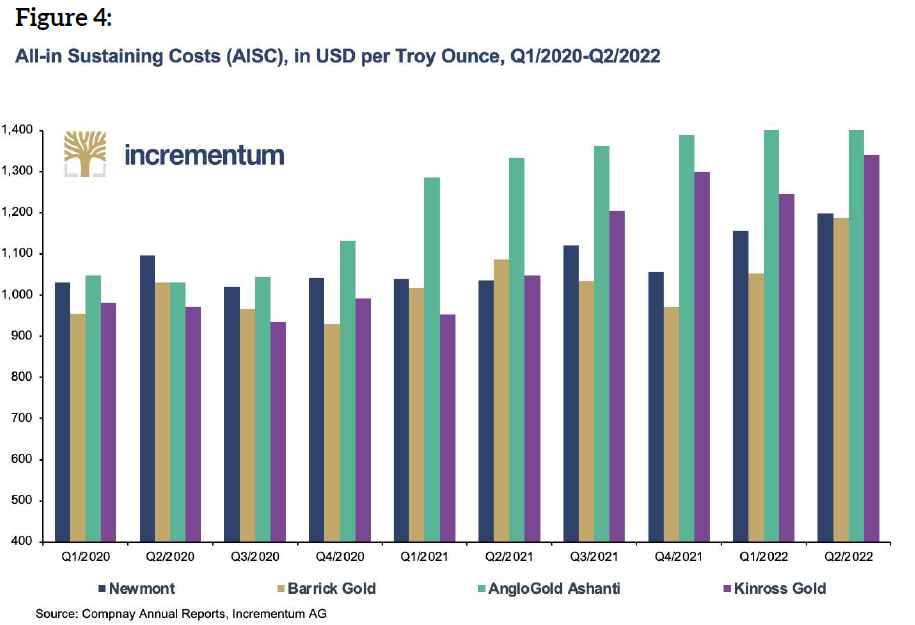

The industry is already feeling the impacts. The table above (Figure 4) shows the development of AISC of major gold producers during 2020 and 2021.

Of course, the higher-inflation environment should be positive for gold prices, which should compensate for the higher capital and production costs. But there is no guarantee that the gold price will increase enough to fully offset the higher costs.

Conclusion

The main reasons for the underperformance are CAPEX overruns, growing production costs, problems with obtaining permissions for new mines, governments wanting a bigger share of the pie, political instability in some countries where gold mines are located, as well as declining reserves and numbers of new discoveries. As not all of the miners are impacted by all of these factors and not equally, it is important to choose the right company when making a long-term investment in the gold mining industry.

The best strategy is to buy shares of a company operating in a safe and mining-friendly jurisdiction, with low production costs, reasonable CAPEX, and good exploration potential.

1 This is an updated and highly abridged version of the original article, which has been published in the In Gold We Trust report 2022 that you can download for free at https://ingoldwetrust.report/?lang=en

2 We did discuss this problem in: “Mining Stocks: The Party Has Begun,” In Gold We Trust report 2020

3 See “Gold Mining Stocks –After the Creative Destruction, a Bull Market?,” In Gold We Trust report 2019

4 See “McKinsey presents ‘mega project’ blowouts and how to avoid them at PDAC,” im-mining.com, March 6th, 2019

5 See “Gold Price Framework Vol. 2: The energy side of the equation – Part II,” goldmoney.com, July 10, 2018

{kind=link}