Lithium plays a critical role in electric vehicle (EV) batteries and in the energy transition overall, and a significant amount of metals and minerals are needed to accelerate and maintain the momentum of this transition. However, miners, investors, and those in the downstream market, such as automakers, are still trying to determine how much supply we will need in the coming years and where it’s going to come from.

Looking at lithium, the price of the metal has surged significantly over the past year as EV sales globally have accelerated and the demand for this critical battery metal has increased (alongside mounting market anxiety about its availability). Benchmark Mineral Intelligence (BMI) has noted that the price of raw spodumene rose 478.3% from January 2021 to January 2022, and that similar increases in price were recorded for lithium carbonate and hydroxide during this time.

BMI is also forecasting that the price of lithium will continue with this upward trajectory for at least the next six months. Analysts note that lithium pricing can be quite volatile though – demand can grow quickly and then as new mines open and bring the supply back up, the price can easily drop again.

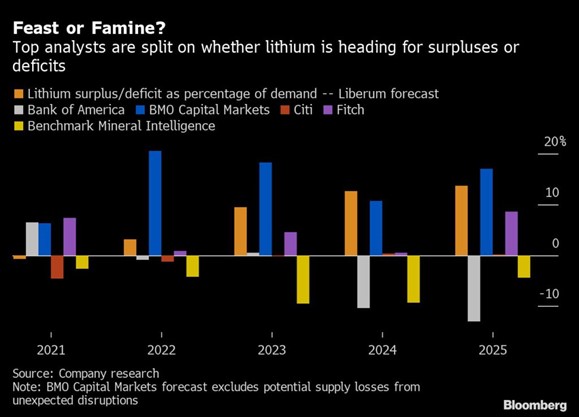

While the demand for lithium continues to grow at a strong pace, there is no clear consensus on what supply will look like down the road. In a survey of some of the leading lithium analysts, Bloomberg notes that estimates for the market range highly – from a deficit of 13% of demand to a 17% surplus.

This broad range of opinions is in part due to lithium being a relatively small market. Between 2021 and 2025, estimates for the annual growth of the market are around 20% for both supply and demand.

When you compare these figures with the typical growth rates in larger and more mature markets, such as copper, the typical growth rates are more like 2-4%. These forecasts are important though as banks and other financiers use them to predict market movement and in valuing loans to mining and other projects. And for the automotive sector, higher lithium prices and a shortage in supply could seriously disrupt the move to all-electric.

BMI is also forecasting that demand will outpace supply for the near term, even as production is expected to double its 2021 numbers by 2025. According to the US Geological Survey, global mined lithium production reached a record high of 100,000 tonnes in 2021 – a 21% increase over its 2020 figures. Lithium production has grown in response to the strong demand from the battery and EV markets, though supply security and regionalized supply chains have emerged in the wake of the COVID-19 pandemic as a growing concern for the market. However, even with the push to grow production, analysts question how nimble the lithium market really is and if we can find a balance for supply and demand.

Andrew Miller, COO of BMI summarized that there is too much optimism about the responsiveness of supply in the lithium market: “It’s very hard to see how it’s going to accelerate at the speed that the battery market and electric vehicles are accelerating,” he said. And so more concrete analyses and forecasts may be needed to accurately gauge future supply and demand as the energy transition accelerates.

{kind=link}