As the world accelerates towards a net-zero emissions future, challenges are becoming increasingly apparent. Wood Mackenzie’s Future Facing Commodities Forum shed light on key factors shaping the future of critical minerals like lithium, cobalt, copper, nickel, and rare earths. Here are five challenges that define the trajectory of the global shift to clean energy:

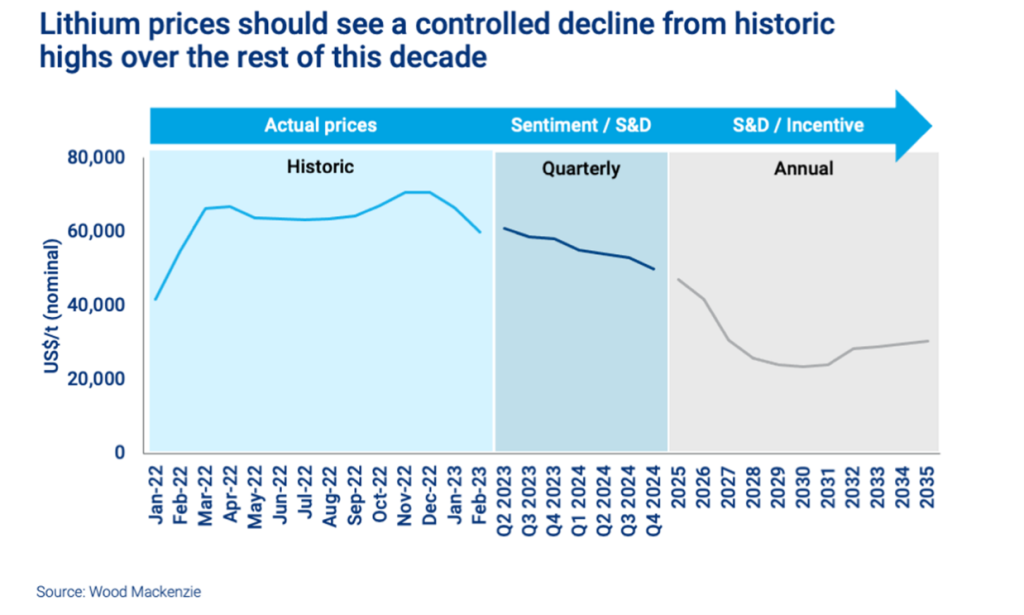

1. Balancing Growth: The global market for critical minerals is marked by supply imbalances abruptly swinging between deficit and surplus. The lithium market, in particular, exhibits these characteristics, indicating an immature market. The skyrocketing demand for these materials, driven primarily by the surge in electric vehicle (EV) uptake, has strained the supply chain. With rechargeable batteries driving approximately 85% of global demand, the surge in EVs has created a skyrocketing demand for lithium. The development of mining and refining infrastructure, however, requires significant investments and time causing it to struggle keeping pace. This imbalance caused lithium prices to soar in 2022 but subside in 2023. Going forward, prices are expected to experience a controlled decline, settling at around US$20,000/t by the end of the decade.

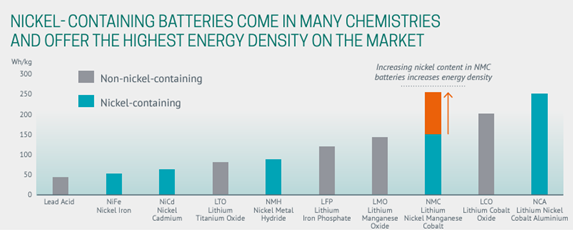

2. Ensuring Quality: The quality challenge extends to critical minerals like nickel, which play a crucial role in the global shift towards clean energy. Lithium-ion batteries using nickel-rich cathodes require high-purity nickel, typically in the form of nickel sulphate. However, most of today’s nickel production, such as nickel pig iron (NPI) or ferronickel (FeNi), is not suitable for battery-grade nickel sulphate. These requirements necessitate the exploration of alternative refining processes and sources in order to meet the stringent quality requirements. Collaboration and investment in research and infrastructure are crucial to optimize refining techniques and ensure a sustainable supply of high-quality nickel and lithium for clean energy applications.

3. Dissecting the Market: Critical minerals used in battery compositions are not simply one product under the umbrella term for an elemen[EL1] t. The lithium market encompasses two primary products: lithium carbonate and lithium hydroxide. The choice between the two depends on the cathode chemistry used in batteries. Lithium carbonate is driven by lithium iron-phosphate (LFP) batteries, which are widely adopted in the Chinese market and gaining popularity elsewhere. On the other hand, lithium hydroxide is favoured by premium EV manufacturers due to its compatibility with high nickel cathode chemistries like nickel-manganese-cobalt (NMC) and nickel-cobalt-aluminium (NCA), offering higher energy density. This distinction has implications for the pricing of both compounds.

4. Uncertainty in Long-Term Supply: While projections for critical minerals supply can be made based on existing, planned, and potential mining projects until the end of the decade, visibility becomes less clear after 2030. For instance, assuming a supply of 1.5Mt of lithium, the cost would be around US$15,000/t (however, market pricing is expected to be higher). This uncertainty makes it difficult to determine future supply and pricing. If prices aren’t attractive enough, it may discourage new mining projects. This poses a risk to the availability of critical minerals for the clean energy transition. Collaboration and strategic planning are needed to ensure a stable supply. Efforts like diversifying sources, promoting recycling, and investing in alternative technologies can help address these challenges.

5. Market Immaturity: The future of the lithium market presents a significant challenge to many climate goals worldwide due to its early stage of development. Unlike more established markets, there is currently no globally accepted standard for lithium products, making it difficult to determine pricing benchmarks. The uniqueness and precise specifications required for lithium products bring about a pricing complexity comparable to that of specialty chemicals. However, the industry’s focus on meeting growing demand restricts it from taking the opportunity to pause and establish a more uniform and consistent approach to pricing. It is expected that greater standardization will emerge in the future, but this process will require time.

As the global energy transition progresses, understanding these challenges, from supply fluctuations to quality considerations, will be pivotal for governments, stakeholders, and mining companies navigating the evolving landscape of electrification.

Going forward, partnerships will play a crucial role in shaping the future of multiple critical minerals industries. Collaborations between miners and refiners will likely become prevalent as companies seek to share risk and capital requirements.

By addressing these obstacles head-on, we can pave the way for a smoother and more sustainable transition to clean energy.

{kind=link}