On 29 July 2023, the New York Times published an article entitled Coast to Coast, a Corridor of Coups Brings Turmoil in Africa, which reported on the emergence of a continuous chain of countries stretching across the continent that had experienced a coup during the 2020s. This chain has been named the coup belt and encompasses Guinea, Mali, Burkina Faso, Niger, Chad, and Sudan. The first of these occurred in Mali in August 2020 and the most recent in Niger in July 2023.

Since the first coup in late 2020, Africa-dominant gold miners have largely underperformed relative to their Australian peers. We believe that all African gold miners are being unfairly painted with the same brush, with some investors assuming that all gold miners in Africa are subject to similar socio-political volatility to those in the coup belt. Below we provide a company specific comparative analysis to illustrate this.

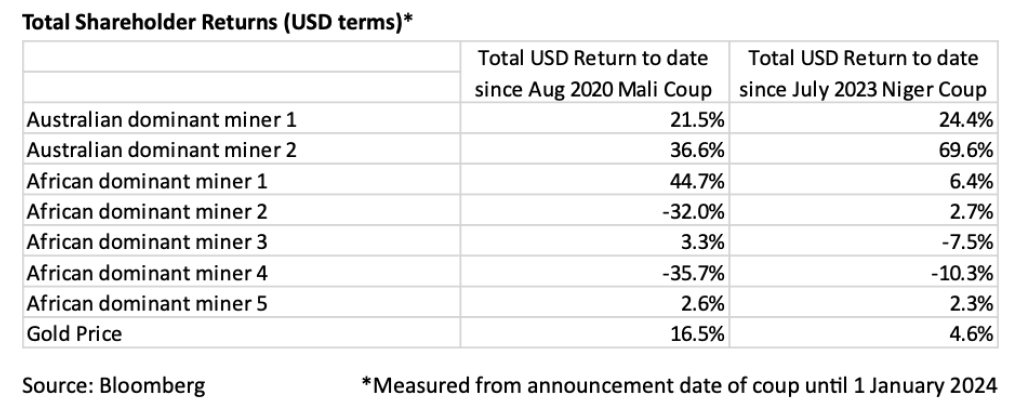

The case study uses a group of listed, multi-asset, gold miners which have industry leading corporate governance and business management practices. The only difference between the companies is the location of their mines. Since the initial coup in Mali, Australian gold mines have generated a total USD shareholder return of 29%, a 32% outperformance over African gold mines.

Only one African gold mine matched the shareholder return performance of its Australian peers, however, this proved to be fleeting. The latest coup in Niger was the final straw, with all African gold mines underperforming compared to Australian mines by almost 50%. This is despite the fact that some do not operate in any of the countries in which coups have occurred.

Many investors are unfairly categorizing all African gold mines in the same manner, viewing them all as subject to the same socio-political volatility. Sustainable Capital takes a company-specific approach when performing investment due diligence on all of its portfolio investments. When analyzing natural resource companies, we focus on the following key metrics amongst others: asset quality, sanctity of property rights, and valuation.

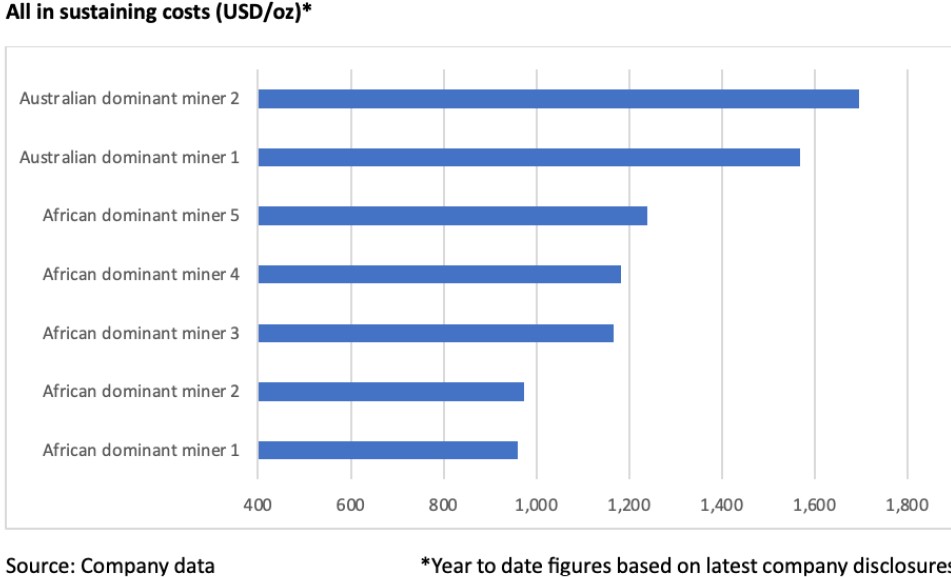

In our view, the best measures of asset quality are life of mine and all-in-sustaining cost (AISC). The average life of mine (based on reported reserves) for African gold mines is over 10 years, which is largely in line with Australian miners.

However, this is where the quality similarities end. Australian gold mines operate in the top half of the global AISC curve, in contrast with African mines, which are in the bottom half. This keeps African gold mines cash positive even at lower gold prices.

Large scale commercial gold mining in Africa has a long history with fiscal arrangements along with mining laws, which have remained stable despite a dynamic socio-political environment. Something which contrasts with Australia, where the operating environment has been more volatile and challenging.

Africa’s natural resources are an important facilitator of development on the continent, which should have a net-positive impact on all stakeholders

This is reflected in the Fraser Institute’s latest annual survey of mining companies, where Australia’s major mining regions have recorded declining scores in their Investment Attractiveness Index, while African countries have seen a general improvement since 2018.

Furthermore, the gold mining industry in many African countries makes an outsized contribution to government budgets, economic development, job creation, skills transfer, and rural community development.

Ultimately, the market price should reflect the quality of the company’s assets, their business practices, and the relevant sovereign risks. The blanket approach that has been applied to African mining companies ignores this principal.

We estimate that market prices imply a risk level for African companies that is two to three times that of Australian equivalents, even for those in countries not subject to coups. The risk differential implies that investors are assuming a worst-case scenario (i.e., mine nationalization and regional conflict) for the entire continent, which we believe is unlikely, even for those countries which have undergone regime change.

Placing all African mining companies in the same category has created an unusually compelling opportunity to invest in low-cost, long-life mines which have globally leading corporate governance and sustainability business practices at unjustifiably distressed market prices.

At Sustainable Capital, we continue to believe that Africa’s natural resources are an important facilitator of development on the continent, which should have a net-positive impact on all stakeholders. We believe that a company specific approach to investment due diligence can demystify the inherently negative news headlines and highlight the investment potential of high-quality African gold miners.

{kind=link}