The planned transition of our world from current 4.3t1 CO2 per person to net zero by 2050 will require a dramatic increase in renewable energy, transport electrification, and battery storage. Annual capacity additions of wind and solar energy will need to increase by 2.9x2 and 2.6x2 respectively by 2040 to 320 and 160 GW. Global Electric Vehicle (EV) penetration is expected to reach 12% by 2030 with 230M3,4, EVs expected to be on the road by then.

All in all, the energy transition will require an incremental annual copper production of 10mt4,5, by 2040 (~8 new Escondidas), driven by renewable energy, required grid upgrades, and EVs and their charging infrastructure. The energy transition, however, isn’t the only driver for copper demand. When including other demand drivers, an incremental 15.2Mt4,5 annually in primary mined copper is needed by 2040, and this assumes an almost 1.7x6 fold increase in copper recycling.

Depleting deposits and declining grades also need to be replaced with new supply, and the last large new copper deposit (Kamoa) was discovered 13 years ago. Most large new projects face permitting, technical, country or community challenges, and even successful projects most of the time require many years of permitting and development until they are in production. It is far from clear where the required new copper supply will come from.

The same supply crunch is expected to repeat itself in other metals and minerals. In lithium, more than 1400%2 increase in annual supply is required over the next 20 years, in nickel 170%2, in certain rare earths elements like neodymium 180%2 etc. All these projections already consider a significant increase in recycling. Given the difficulties in getting any mining project off the ground, there seems a real risk that the energy transition to zero carbon will not be achievable for lack of raw materials.

High prices will benefit investors, but beware the development risk

The result will be higher prices which will benefit investors but which will ultimately be borne by consumers. Junior explorers targeting metals required for the energy transition, as well as investors in producing companies, will be the main beneficiaries on the public markets. A big question mark, however, looms over the financing to develop the required new projects into production. The required project pipeline in most metals and minerals simply does not exist, when one considers permitting and community realities, technical complexities, lowish grades, etc. In the face of the obvious need for many new mines, there will be strong incentives to “roll the dice” and try to develop mines that are lower grade, have technical challenges, or country risk and community issues. Especially if inexperienced investors get drawn into the development risk, significant misallocation of capital is likely to happen.

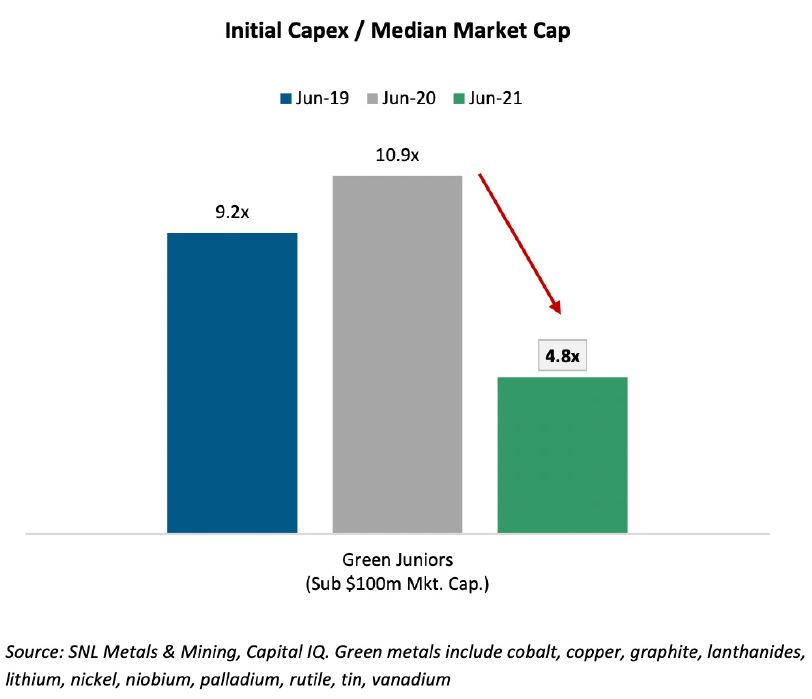

Investment into the development risk requires thoughtful and experienced investors who can ascertain which projects are likely to succeed, and those skilled investors who base their decision on correct technical underwriting, will achieve significant returns. Development might, irrespective of demand, remain constrained by financing since the development capital required relative to the market caps of companies is on average still very high. For example, the chart above shows that even now, after dramatic share price increases, junior miners focused on energy transition metals still need to raise 4.8 times more capital to develop their projects than the underlying companies are worth.

Investors also should not forget that battery metals are exposed to significant risks. While lithium, for example, is the most frequently found metal in the earth’s crust, there are only a few lithium deposits that meet the requirements for commercialization in terms of grade, scale, location, and proven technology.

Metallurgical coal misunderstood, gold mining under potential threat?

While a supply deficit in a significant number of metals and minerals is the most commonly discussed impact of the energy transition on mining, there are some more nuanced themes emerging, that investors should be aware of.

Metallurgical coal, for example, will likely face an almost blanket ban on permitting and financing of new supply. This is driven by a lack of differentiation between thermal coal (used for power generation) and metallurgical coal (used for steel production), but also due to a lack of understanding of the metallurgical coal sector.

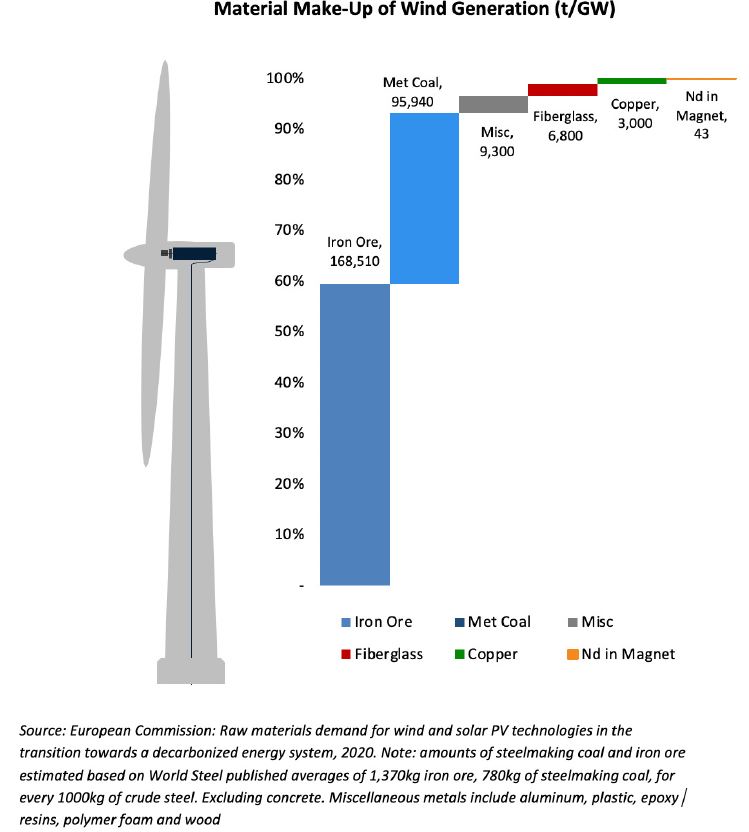

Only 8% of CO2 reductions in the steel industry over the next 30 years are expected to come from hydrogen, while 40% are expected to come from more efficient raw material input into the steelmaking process. Metallurgical coals that sit in the bottom quartile of the scope 1 and 2 emissions curve will and should play an important role in helping steel mills reduce their CO2 footprint, by replacing high CO2 coals in the blast furnace, and the demand for these “low CO2 coals” is expected to triple within the decade. This expected demand growth combined with ideologically suppressed future supply is likely to lead to much higher long-term prices and makes certain types of metallurgical coal one of the best contrarian bets available in the market.

Uranium is for many investors also a no-go area, although it seems obvious that nuclear energy will play an important role on the journey to net-zero. The question is when that point of realization will come on political and societal level such it translates into increased demand and sustainably higher prices.

Lastly, in a world where every new mining project has to justify its development, not only economically and environmentally, but also increasingly on the basis of its CO2 footprint, forward-looking investors might become wary of the gold mining sector. It’s easy to see how in the not-too-distant future the same ESG activism that is currently directed against coal, could take gold mining into its crosshairs. The author of this article already encountered critical ESG-related commentary about gold mining: why emit CO2 into the atmosphere by building and operating mines that produce a metal that has barely any utility in the real world? Almost every ounce of gold produced is still lying around somewhere above surface, mostly in a safety vault, without broader industrial use. This argument might be hard to refute.

On the basis of its CO2 footprint, forward-looking investors might become wary of the gold mining sector

In summary, the energy transition represents a generational opportunity for metals and mining. For the public market investor the exploration and production side is probably the best place to be, the development risk on the other hand should be best left to companies and investors who genuinely understand the technical execution risk.

1 International Energy Association – 2021 CO2 ¬Emissions

2 International Energy Association – The Role of Critical Minerals in Clean Energy (2021)

3 International Energy Association – Global EV Outlook (2021)

4 The International Energy Association does not report EV penetration in 2040 however the IEA applies the same modelling principals when it extrapolates the 2030 EV number in its 2040 copper demand modelling

5 Denham calculation based on International Energy Association’s Sustainable Development Scenario and Wood Mackenzie Forecast

Copper Demand Supply Modelling

6 Wood Mackenzie

{kind=link}