Let’s start with some background into you and your work within the metals and mining industry.

I work with Astris Advisory in Japan as a commodity strategist. I’ve been a commodity strategist and analyst for about 20 years now, always in Asia. I was in China from 2003 to 2014, Singapore after that, and then Japan since COVID. I analyze the commodity markets, looking at the bulks, the base metals, and new energy materials, on a global basis.

Historically the big story in metals has been about China and how it’s been driving demand within the industry. What have you seen coming out of China post-pandemic?

The initial years post-pandemic saw a strong rebound in China. There was obviously a lot of stimulus to offset the economic weakness of the pandemic, and that carried through 2022 and into 2023. But this year, we’ve seen quite a drop-off in activity in China. The troubles in the housing market have been quite well-documented, and volume sales have been down heavily since 2020 when they finished their social housing programme. With the private market, they’ve said, “Look, we’ve basically built too many apartments now.” The statistics show that China has actually built more than one apartment for every urban family since 1999. So, it’s about better utilizing what they’ve got rather than building more new housing units.

The other factor is that they have had a big clampdown on local government debts, and therefore infrastructure investment. So, infrastructure activity is really struggling this year. Cement demand is running down about 11%, that’s why steel demand is suffering so much, running down about 5% for this year.

China is struggling in what we call the old economy, but there are still some good news stories in China as well. The new economy, things like electric vehicles (EVs), renewable energy, technology, are all still growing extremely quickly in China. EV sales are up about 30% this year, and power consumption is up over 5%.

There’s a real split now between what I call the old economy, things like steel demand and therefore iron ore, versus the new economy, which is a lot more base metals intensive, and obviously battery materials focused.

You’re quite keen on India’s growth story now. What’s happening there in terms of demand, and why should the industry take notice?

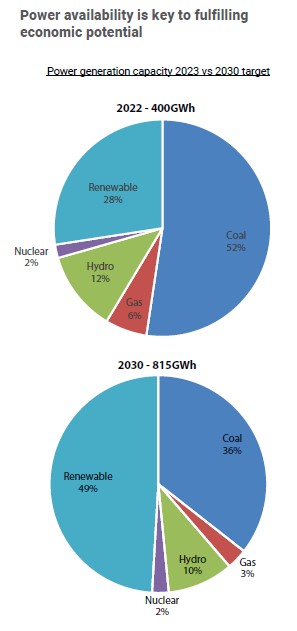

India has really taken off post-COVID. For the last 20 years, there’s been a lot of hope about India, but it’s always struggled to really deliver and fulfill expectations. Modi made a lot of changes early in the demonetization process, bringing all the money into the banks, managing bankruptcy reform, financial reforms, and investing in power infrastructure. Because of this, India hasn’t really suffered blackouts and brownouts since 2019. There was also a lot of investment in roads, ports, etc. So, the country has the infrastructure and it’s got a better financial system. Also, digitization has really streamlined government approvals, processes, all that stuff to speed up activity.

Now, there are three main drivers of growth in India. Number one, government investment. There is massive investment in roads and ports, and now in railways. They want to electrify all the railways. They’re building a Japanese bullet train network, partially funded by Japan. So, that’s the infrastructure side of things with lots of government investment.

India is also building 20M social housing projects and they’re installing solar panels on people’s roofs. One of the things Modi said in the election is the idea of getting free power to the people in rural areas. So, his government started to install solar panels for free. India’s got massive investment plans on renewable energy going from 166Gw last year to over 500Gw by the end of the decade.

Finally, you’ve also got the foreign direct investment (FDI) side of things where Modi has been running around the world trying to encourage more investment. They’ve got this ‘Made in India’ programme. I think India currently consumes about 4% of global goods, but only manufactures 2%. Now, you’re starting to see more and more factories moving to India. Again, that’ll help boost the commodities consumption on both constructing the factories and then operating and manufacturing the goods.

Can you talk a bit about some of those key commodities that are going to be part of this Indian demand story?

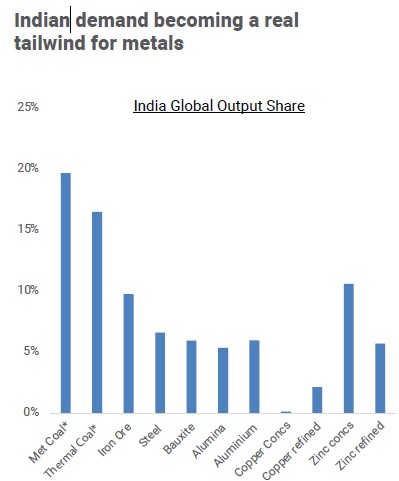

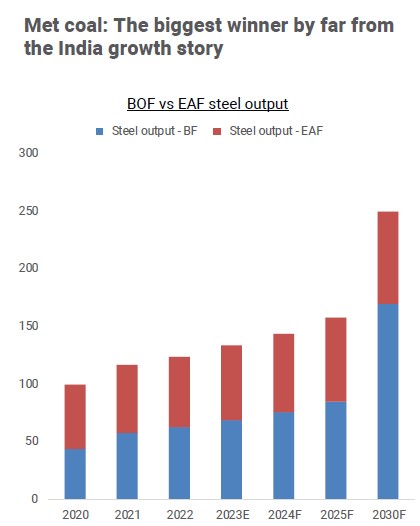

This all boils down to geology. In China’s boom, the key thing they didn’t have was hematite iron ore. With iron ore they had an 85% reliance on imports, which drove the pricing boom there. The story for India is that they have an abundance of iron ore, but barely any metallurgical coal. So, metallurgical coal will be to India what iron ore was to China. India is building about 80Mt of blast furnaces. They’ve only got 80Mt of operating furnaces at the moment, so their metallurgical coal demand could double over the next decade, and India is already the biggest buyer of seaborne metallurgical coal.

Another point is that geologically, India doesn’t have much copper, so that stands to benefit again. They’ll have to import a lot of copper.

Finally, what trends should we be looking out for in the short term?

Short term, commodities have had quite a volatile year. We saw very high prices in May, with copper hitting record highs. A lot of that was AI derivative money coming in and a bit of over excitement on that angle. Whereas now, commodities are back down again, and there’s a lot of pessimism about global growth, growth in the Western world, and a stronger dollar. Nearer term, it’s about the global macro environment, can the US and Europe finally shrug off the recession and see a bit of recovery next year or something that would certainly help? But otherwise, it’s pessimism on China.

My view now is that China is through the worst. It’s been terribly weak this year. Steel demand was down 5%, but I don’t think next year we see another double-digit decline in construction. So, I think it starts to bottom out there and you might see a bit of an improvement into year-end. And of course, India has had one of the longest, wettest monsoon seasons in 100 years. So, activity has been very suppressed in recent months, but India is coming out of its monsoon season now.

Commodities have always had this interesting trade, where you sell in May, buy in September, and that entirely matches the Indian monsoon season. So, as India becomes increasingly significant on the demand side, could we see a bit more seasonality within commodity prices going forward.

{kind=link}