The drive towards decarbonization was for many years the domain of lobby groups, future thinkers, and the stuff of fringe politics. Today, the decarbonization revolution is here, and it is finally real, increasingly supported by government policy, economics, and compelling IRRs. With world governments declaring net-zero targets, ramp-up in large-scale manufacturing of electric vehicles (EVs), and a fundamental shift to renewable energy plants and batteries, we are now seeing the demand that has long been hoped for.

The key metals that are likely to benefit from this huge change are copper, nickel, cobalt, and lithium. Australia has abundant lithium and nickel resources, with some exposure to cobalt production. Chile is a large producer of lithium and copper, and the Democratic Republic of Congo accounts for 70% of the cobalt market and 50% of its reserves.

The two drivers for electrification metals are EVs and renewable energy – both of which are seeing their underlying cost dynamics plunge, making them increasingly affordable for end consumers, and increasingly competitive with fossil fuels. Where EVs were once a luxury item, supported by government policy in a number of countries, customers now have a choice between EVs and internal combustion engines (ICEs) at similar price points. For savvy buyers, EVs add the benefit of at-home charging capacity and can themselves readily source alternative energies like solar power to further reduce operating costs.

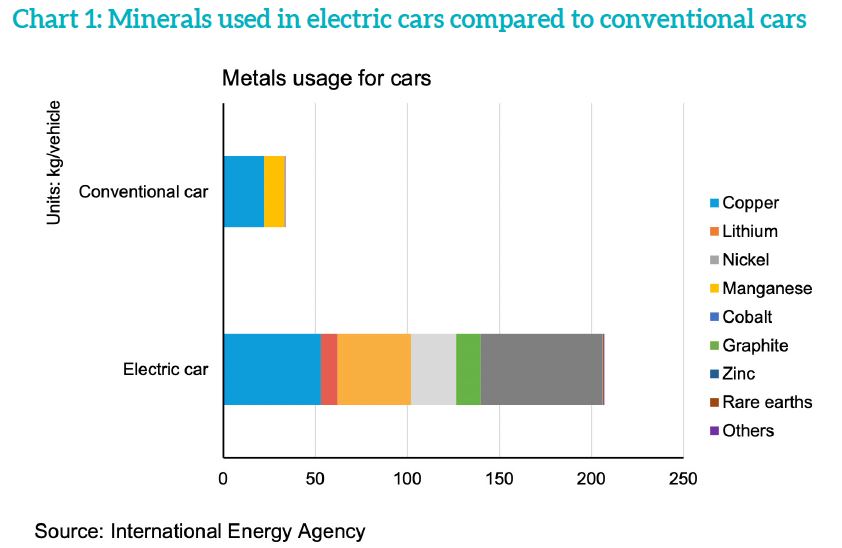

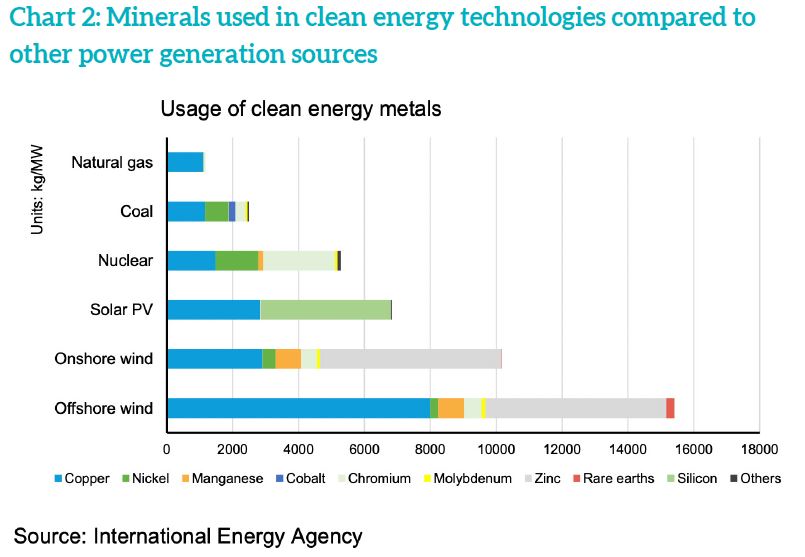

Increased efficiency and mass production is also reducing the cost of renewable power. The good news for the exploration community and commodity investors alike is that EVs and clean energy are heavy users of metals and rare earths, as illustrated in Charts 1 and 2.

The production of EVs consumes more than six times the key minerals and metals by weight than does the production of conventional cars. Of the approximately 207kg of minerals used in EVs, 32% is graphite, 26% is copper, 19% is nickel, 12% manganese, 6% cobalt, and 4% lithium. By contrast, conventional cars use mainly manganese and copper, but in much smaller measures.

The metal and minerals use equation for renewable energy is similar to that of EVs in terms of intensity. If you take coal energy as the baseline for minerals demand for purposes of comparison, for every megawatt (MW) of power produced: half the demand is required on a kg/MW basis for gas energy; nuclear uses more than twice the minerals of coal; solar 2.75 times; onshore wind more than four times; and offshore wind more than six times.

From our perspective, the main commodities of interest in the decarbonization thematic are lithium, graphite, and NdPr. Nickel and copper will also benefit from decarbonization, but this is likely to be longer-dated given the amount of nickel and copper that is consumed by demand sources currently. The demand outlook for electrification and other base metals is very strong, as is illustrated in Chart 3.

Lithium is an abundant mineral, but currently extraction and processing capacity is limited, meaning there is a very tight market for lithium, with demand exceeding supply. The lithium-ion battery is currently the incumbent battery technology, and this is not likely to change any time soon. We see a tight lithium market for at least 12-18 months, potentially longer, as new projects and existing resource expansion are needed to meet growing demand.

Across the lithium space, we see opportunities in both producers and developers

Graphite can come from two sources, natural (mined and processed) graphite and synthetic (manufactured from oil/carbon sources). Synthetic graphite production is energy intensive, and can be environmentally damaging, but typically produces a more consistent product. Natural graphite can produce a slightly lower quality product with less impact on the environment.

Right now, energy constraints in China are seeing constraints on synthetic graphite production, which is supportive of natural graphite prices in the near term.

One area we believe is underestimated by the market is the demand for NdPr, a rare earth used in high-strength magnets. Rare earths magnets are used in energy efficient motors. Because of the very high magnetic strength of rare earths magnets, electric motors use less energy to produce the same amount of power (that is, they employ less electrical power to produce the same amount of mechanical power). This trend is likely to continue, with rare earths magnets in everything from EVs to vacuum cleaners and home appliances.

New mines required

Part of the change that needs to occur with an increasing trend towards renewables is growth in the availability and quality of energy storage. Since renewables can be unreliable, and may not be suitable for base load power, some form of storage is needed to offset the intermittency of some renewable sources. There are many models that can work together to solve the storage puzzle, such as giant utility-sized batteries like that which Tesla installed in South Australia, to fragmented batteries that create a network of energy at the household level, where the home or even the EV is part of the energy storage grid. Much of this technological development is about policy and how it evolves, and a lot will be determined by the behaviour of consumers and technology firms that offer new options not previously considered possible.

To meet the significant growth forecasts for metals from global decarbonization, investment in new mines and processing facilities is required to meet growth targets. Investment is also needed in exploration. This cycle (as with most commodity cycles) usually stems from high commodity prices incentivizing new production (rather than the market preparing for growth, where prices rise drive investment).

What we have now is demand dragging prices forward for these key green metals where supply and mineral development have simply not kept up. We believe this is likely to be a trend for some time as explorers and producers scramble to meet the underlying growth in green metal demand.

Ausbil is heavily invested in the decarbonization theme, with investments in lithium, graphite, and rare earths. Across the lithium space, we see opportunities in both producers and developers, while in graphite, we own an interest in a large-scale developed market natural graphite producer. In the rare earths space, we prefer current producers, as construction and commissioning of new projects is incredibly complicated and faces significant regulatory hurdles.

As is the case where supply undershoots demand, there will be a flurry of exploration and development, mergers, and acquisitions. Exciting as this is, perhaps more compelling is the strong underlying demand growth we expect to see in renewable metals over the next two decades. Unlike many of the boom-bust commodities cycles of the past, these metals may see a more structurally stable demand profile, offering truly long-term compound returns in this space, across the cycle.

{kind=link}