Let’s look at some of the major trends that you’re seeing across the commodities markets at the moment. What’s most of interest?

It’s almost like a two-speed market. We’ve seen a number of things over the past three years which have had real investor attention directed towards them, often because of a spike in a price. But, in the last three years, we’ve seen most of those round over their top and then come off.

Most of the main commodities like copper, iron ore, etc., have softened between 2023 and 2024. Commodities have generally been weak. On the flip side, you’ve got gold which has had some buying behind it because it’s been hitting new record highs. That should be fantastic for gold miners and gold equities, but I suppose that’s where it breaks down because we haven’t quite seen the investor attention that I would have expected towards gold in a robust gold price market.

So, there’s some great reasons for that, but I suppose they’re the high level commodity trends.

You mentioned these high gold prices, especially over the past year. Do you think these prices are here to stay? Where do you see the market heading?

I think gold prices have been provoked by buyers out of the East. People talk about central bank purchasing and, yes, the Chinese Central Bank has been very prominent in that in the last 18-24 months. So, that’s an obvious source of buying.

The Chinese retail investment market had also mimicked that to some extent. But there is buying from a lot of BRIC nations, which has been pushing up the gold price. Over much of that period, the Western ETFs had been sellers of gold and, traditionally, for the last 20 years or so, they’ve been the price setter for gold. If the ETFs are buying, the gold price would go up. If the ETFs are selling, the price would go down.

So, you’ve got this East versus West scenario. You’ve got the Western market, which hasn’t been a believer of gold, and the Eastern market, which appears to be. And the Western market is what is pricing gold equities primarily. So, that’s where you see the breakdown.

Where’s that going to go? It’s interesting that the Eastern market has been so robust, and that makes me sit up and take notice. That falls against the backdrop of two things. First, the invasion of Ukraine via Russia led to US dollars being confiscatable assets. And that point in time is where you’ve seen this amazing Eastern interest come into the gold market. That’s one key factor that we’ve seen which has caused a massive breakout in the gold price against the factors which have been traditional correlators.

The other interesting thing, is that this happens against a backdrop of flat production growth globally in gold. So, for the last five or six years, production growth in gold has been negligible. It’s gone up and down a bit. These flat spots in gold production that we’ve seen historically have often corresponded with the start of a gold bull market. It’s a simple supply versus demand argument but it doesn’t get talked about much in gold because there’s always this looming idea that if the gold price goes up, then people will start to liquidate their gold bar investments, but I don’t think we typically see that.

Usually, gold buying interest is met by production out of the ground and when that is flat, then it can put a little bit of an upward pressure under the price. With those two things corresponding, it’s difficult to say what the gold price should or would be, but it looks as if it should go on to be positive from here on.

Since you also look across the commodity spectrum, can you talk about some of the key points of interest in other markets?

I think gold, up, and the rest of the commodities, down, is a feature. There are spectacular long term demand fundamentals for just about all the consumable mineral commodities.

Copper ties itself well to the old and the new world, which features strongly in the energy transition. Things like silver go into solar panels. So, for a world which is generating more and more from renewables, that should feature well. Then, you have uranium, which is a great source of energy and is carbon neutral. Once you’ve built your processing and generating facilities, uranium doesn’t contribute any carbon dioxide emissions.

All of those have the two biggest economies in the world questioning them and their long term growth.

One of those economies, the US, has an election coming up in November. Probably one of the biggest question marks is when Donald Trump potentially comes back into power. He talks about what his policies are, and he has a track record. But does that paint itself as a positive? I’m not entirely sure, particularly from a global economic perspective. The US might perform differently under him, but will that be good for its position within the global economy? We’ll just have to wait and see.

The Chinese economy is the other one, and is really cracking under a history of needing to provide stimulus to keep their economic growth going, but it looks as if the willingness and capability behind that is falling, and so, the Chinese market doesn’t really believe in itself that much at the moment. I think it needs to solve some problems within its real estate market in order to show itself as a big consumer going forward.

So, with those two factors in place, the next 10 years look fabulous from a commodity consumption point of view. But, the next 12 months do look a bit problematic and that just aligns with a typical commodity cycle. We’ve been in a down leg recently. We know that after you go through a commodity bust, you get back into a boom. So, I think the long term looks quite encouraging, we’re just in a period of slowness in the meantime.

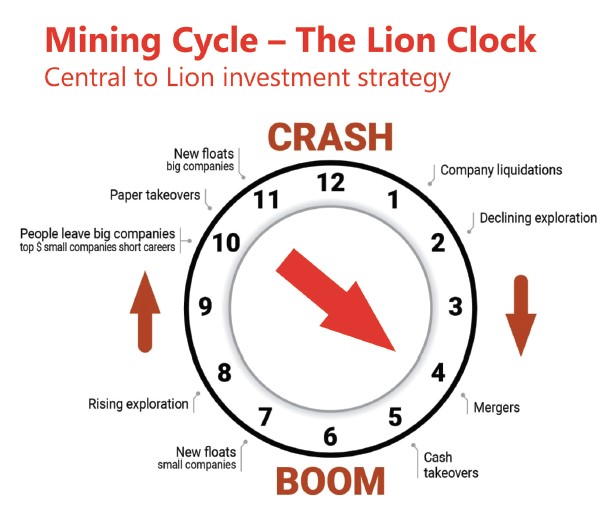

Can you can talk a bit about where the markets are now in terms of positioning within the Lion Selection Clock?

12 o’clock would be the absolute top of the boom. We were calling that in early 2023, and in retrospect, looking back over charts, it was more accurately sometime early in 2022.

That puts us around 2.5 years into a down cycle. This has been felt most strongly by the juniors, micro caps, and explorers, probably more so than in previous cycles. In this case, it’s been overprinted by the risk appetite of an equity market which has avoided small caps. It has pushed money into the large, more sure plays in the market.

So, that’s benefited the BHPs and the Rio Tintos of this world, and enabled them to outstay some of the commodity price fluctuations that we’ve seen. But, with most commodities looking like they’ve had their peak pricing already, we’ve seen BHP, Rio Tinto, and others also come down, they’ve been in a downtrend as well.

We’re saying we’re at four o’clock now, with six o’clock being when you would round off the bottom, and go into the early stages of the next boom.

I think between now and 6 o’clock, we need to see some level of capitulation where you can say commodities have gotten to a bottom and the major equities for BHP, Rio, etc., also get to a bottom. Some of the factors are going to relate to whether or not we see some of the large tech stocks having capital rotate out of them and what sort of impact on the global equity market the US election and concepts of US and Chinese recession play into that. Give that a year or two, and I think we’ll be well on the other side of it.

You’re focused mainly on investing within the ASX junior market. Are you seeing any positive opportunities there?

We invest in the smaller stocks in that space, essentially the subset of ASX-listed resources companies that are capitalized at less than A$250M market cap. There are an awful lot of companies that fall into that basket, and their prices are down by about 75% in the past two years.

We’ve been investing most aggressively in the last six months. Not because we see that we’re at the bottom, but because we think that within the next year or two, we’ll go through the bottom.

So, there are a lot of opportunities. First, it was gold. That’s where we saw the best value early on. We’re also starting to see fantastic value creep into the critical mineral space as a lot of those equities have come well off of their peaks.

To see the value, you’ve got to see a project which you think is going to work at some stage in the future. There are a number of those which we like, and we’re seeing the pricing being very attractive. There are lots of opportunities at the moment.

We’re being contrarian. And the reason we feel that we can be contrarian, is we’ve got ample liquidity to be able to stay agile through an extended period of building those positions. A lot of investors are facing liquidity issues, rather than being able to deploy. So, we’re very fortunate.

Can you provide our readers with some closing thoughts on the commodities markets for the year ahead and what we can be on the lookout for moving forward?

I’d be on the lookout for new sources of demand coming into the market and having an impact on prices so they start to kick up. Outside of gold.

Copper, iron ore, some of the bigger markets, do have a bit of weakness taking us into 2025. But as we as we go through that electoral cycle in the US in particular, and into 2025 and new policies start rolling, I think that’s where you could start to see some consumption trends changing direction and heading positive again.

But 2025 is going to be a year where we see a lot of those things turn the corner. We’re going to see new iron ore supply come online in West Africa. I think that’s probably going to be tough for the producers of iron ore in the rest of the world, because that’s going to be cutting their lunch a bit with new supply going into a fairly static demand market. It will have an effect on price. But we don’t see that in many of the other commodities.

We’re also seeing a lot of the majors look to strongly pivot their revenues towards copper, and I think that’s because they see that as a market which is going to be pretty firm going into the future. So, whilst it’s been soft this year, 2025 is time to look for a bottom in copper as well.

{kind=link}