Luisa, what is your interest in strategic metals / rare earths?

I started covering strategic materials as an Equity Research Analyst at investment banks in Toronto. Although I covered precious and base metals at the beginning of my analyst career, the increasing relevance of strategic metals for the global economy and investors interest have led me to specialize in strategic materials. Now at Tahuti Global, I follow the strategic metals space, and we offer research and other services in the sector.

Tell us a little about Tahuti Global.

Tahuti Global is a consulting company in the sectors of minerals and material, energy, manufacturing, and technologies. The services we offer include: asset due diligence, financial analysis and evaluation, company, industry and commodity research, value addition, and supply chain analysis. Our clients include mining and technology companies, investments funds, and government institutions. The company was founded in 2014 and we have been very fortunate to attract clients that understand our unique strengths and appreciate our work and contributions.

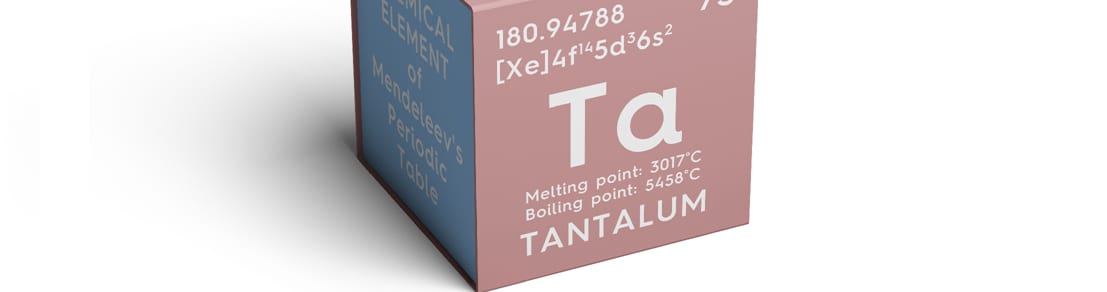

Among the major strategic metals, what is your most favoured metal, and why?

All of the strategic metals are important as they are used in many different and specific strategic applications, but my favorite metal is tantalum. Tantalum’s major application is in the electronics industry, where it is used to make capacitors and semiconductors. As an inert, corrosion resistant, high melting point material, it is also successfully used in pharmaceuticals, aerospace, and defense industries. However, there are only a few successful tantalum mines and there are no listed pure play tantalum companies that could give exposure to investors.

And what is your least favourite?

I don’t really have a least favorite metal, but there are some metals that I don’t follow as closely, like magnesium. I have only received a few inquiries from investors about magnesium and, as such, it has not received much love, so at Tahuti Global we have not written much about this metal.

Can you provide a prediction of where some of the main EV metals (lithium, cobalt, copper) will go in 2019?

That is a tough question. It depends a great deal on the global economy and the EV policies around the world. The situation in North America, for instance, is not the most favourable for EVs at the moment. The trade conflicts between the US and some of the countries that supply key refined metals used in EVs, like China and Canada, is likely to affect prices and supplies of raw materials and parts that are essential for the manufacturing of EVs. China is a significant supplier of lithium, graphite, cobalt, and rare earths (NdPr), and Canada is a major producer of aluminum and cobalt. Moreover, the US government’s decision to relax fuel economy standards for carmakers favours combustion engines, and in Canada, the termination of the electric vehicle rebate program in Ontario, Canada’s most populated province, is affecting EV sales. The main market for EVs should, however, continue to be China. Although most of the car batteries in China are currently the LFP (lithiumionphosphate) type, there is an effort to change it to the NMC (lithium-nickel-manganese-cobalt) type, which should support cobalt as one of the most critical metal for EVs, at least in the foreseeable future, unless there is a change in battery chemistry. Copper prices are still being influenced primarily, by its current non-EV applications, but in terms of copper projects and junior copper companies, I think we should continue to see an increased interest from prospectors and long-term investors, especially for those projects with cobalt by-product.

Are there other metals that deserve mention as well?

Rare earths continue to be critical especially because China is still the most significant producer, and rare earths magnets are very relevant to the EV movement. Other interesting metals include: niobium, which is important in steel making and because production is controlled by Brazil (~85%), refined manganese for batteries, and scandium (sometimes associated with rare earths) that has amazing alloying properties, but has limited production.

What are the main obstacles for REE project developers to overcome in order to bring their deposits into production?

Processing technology is the main obstacle. It will take years and I think it deserves governments’ attention and support, as it is highly risky, expensive, and time consuming. The capital market’s attention span is not very suitable for the development of rare earths projects. The private sector, in collaboration with governments in the West, would have to make a concerted effort to bring about competitive technologies for the refinery and metal making of rare earths.

What do you look for in a potential strategic metals investment in the junior mining space?

It really depends on the metal, but in general terms it is important to understand the mineralogy and processing at very early stage. Resource size and grade are important, of course, but as we have learnt with rare earths, even if a deposit has one billion tonnes of resource and has highly valuable elements, it may not be economic if the materials are expensive to extract and refine.

What is your analysis on Rare Earth Element (REE) deposits across the globe? Which countries hold the most promise for the development of REE projects?

I think many of the rare earths projects around the world are at comparable development stages, some with defined measured resources and advanced economic studies, but most are facing processing challenges. I think South America, Australia, and some countries in Africa have some of the most promising projects. CBMM (Companhia Brasileira de Metalurgia e Mineração) in Brazil has a REE pilot plant and has produced mixed REE chemical concentrates as a by-product from their Niobium tailings. Northern Minerals in Australia has been successfully funding the project’s pilot plant, and is currently in plant commission phase, which is expected to reach full production at some point to study the economics and determine project viability. In Africa, the high-grade bastnaesite deposit is being managed by Rainbow Rare Earths, who are mining and selling REE ore. According to economic studies completed by Canadian junior companies, it seems that Canadian projects are, in general, more capital-intensive, and most have minerals that have never been used for the economic production of rare earths. The minerals that have been economically processed for the recovery of REEs are bastnaesite, monazite, and xenotime. There is potential, however, to produce REEs from phosphate and uranium operations in Canada, but it may not be economically attractive for the major companies.

Do you believe that REE supplies will be used as a tool in the US-China trade wars if there is no agreement? What kind of impact will the trade war cause the REEs market?

I don’t know if the US government understands that there aren’t many other options for the purchasing of refined rare earths products. If they impose taxes on rare earths from China, it will affect industries in the US that depend on rare earths, particularly the petroleum and defense industry. Lanthanum, which is used in the oil refinery process, is the most imported material in the US and China is currently the major supplier. China is still in the process of tackling illegal production of rare earths, and will continue to set up production quotas to domestic producers. However, I don’t think China has any interest in completely blocking rare earths exports to any country. As for now, China has significant control over the processing technology, metal making expertise and production, and is also the largest consumer.

Luisa Moreno

Managing Partner and Analyst, Tahuti Global

Luisa Moreno is managing partner and analyst with Toronto-based Tahuti Global. She covers industry metals with a major focus on technology and energy metal companies. She has been a guest speaker on television and at international conferences. Moreno has published reports on rare earths and other critical metals and has been quoted in newspapers and industry blogs. She holds a bachelor’s degree and a master’s degree in physics engineering, as well as a Ph.D. in materials and mechanics from Imperial College, London.

{kind=link}